This article was first published on the WeChat public account: Zeping Macro. The content of the article belongs to the author's personal opinion and does not represent the position of Hexun.com. Investors should act accordingly, at their own risk.

Core point of view:

From 2012 to 2015, the market has been cleared, and the supply-side reforms have been superimposed in 2016-2017. The profitability of steel mills has continued to improve. The compliance capacity is basically full-load production, the capacity utilization rate has been greatly improved, and equipment overhaul has been neglected, making safety accidents Inevitability in chance. In September, the State Council Security Committee will conduct a comprehensive inspection of the national safety production inspection. The steel factory overhauls the environmental protection and production limit, and the winter production is limited to production and production. The price of the cycle products has remained at a high level for a long time, and the profit improvement of the enterprise has exceeded expectations. Considering that new capacity continues to be constrained, exports are recovering, and demand is flat, we maintain economic long-term judgments.

From the recent market performance of the structural bull market, bond market adjustment, RMB exchange rate strength, and commodity growth, the new cycle is logically and self-consistently verified. After more than six years of market clearing, superimposed supply side reform and environmental supervision, the Chinese economy is standing at the bottom and starting point of the new cycle. The core of the new cycle is: the third phase of the production cycle, production capacity clearing, industry concentration increase, the remaining is king, corporate profit improvement, bank non-performing rate decline, balance sheet repair, accumulation of energy for a new round of capacity expansion .

Downstream supply continued to grow and export recovery continued. The sales of 30-city real estate sales narrowed year-on-year. In September, it was -51.5% year-on-year, down 10.8 percentage points from August. The land supply in September continued to rise year-on-year. The land supply of the 100 largest cities increased by 57.9% year-on-year, higher than that of August. 44.3%; in August, the retail market started to rise, and the growth rate rebounded; the downstream demand for textile clothing increased partially, the market sales were expected to be good, and the year-on-year growth rate continued to rise; the container freight rate index slowed down year-on-year, and the domestic and international freight prices continued to increase. As the price rises, the growth rate of the BDI index continues to rise. It closed at 1250 points on Wednesday, up 35 points or 2.88% from the previous trading day, and rose for three consecutive trading days.

Coal consumption in the middle reaches increased, and machinery sales continued to be hot. Coal consumption in September increased by 21.8% year-on-year, up from 13.2% in August. The average price of rebar rose by 2.0% this week, and the price of rebar in September was 68.1%, up from 61.3% in August. Steel production is likely to rise and fall, and steel production is likely to rise and fall. Cement prices rose 0.4% month-on-week this week, up 24.4% year-on-year in September, down from 27.4% in August. Last week, the national cement storage capacity reached 65.3%, lower than the previous value of 66.0%. In terms of crude oil, after the hurricane, the demand of the US refinery rebounded. The superimposed Russia hinted that the agreement on the reduction of production again would be favorable. The price of crude oil fluctuated upwards. The global economic recovery, China's supply-side reform and the weakening of the US dollar affected the overall increase in non-ferrous prices. According to the data of the Mining Machinery Branch of China Construction Machinery Industry Association, 91,439 sets of excavation machinery products were sold from January to August, a year-on-year increase of 101.1%. A number of factors, such as infrastructure pull, replacement demand, low base effect last year, and export growth, have combined to provide momentum for continued high growth in sales of excavators this year.

The price of pigs has stabilized, the renminbi has strengthened, and short-term interest rates have fallen. In September, the price of fresh vegetables and pork prices stabilized. The National Development and Reform Commission warned that the supply of pork in the second half of the year may increase further. The overall price of pigs will continue to decline, and the growth rate of Chinese herbal medicines and refined oil products will slow down. The central bank restarted its 28-day reverse repurchase operation on Wednesday, and continued to increase its RM298 billion MLF on Thursday to ensure a clear intention for cross-season funds. The R007 interest rate was 3.1391% this week, down 21.83 BP from last week; the DR007 rate was 2.8116%, down 12.92 BP from last week; the 10-year bond yield was 3.6554%, up 2.01 BP from last week. The renminbi continues to strengthen.

Risk warning: Fed rate hike exceeded expectations; domestic currency tightening and financial deleverage exceeded expectations; real estate regulation is too tight; reform is lower than expected; debt risk.

1. Downstream: The supply of land continues to grow, and the recovery of automobile sales is expected to continue.

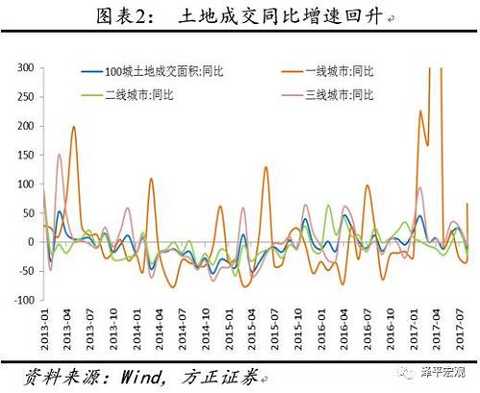

This week, 30 large and medium-sized cities real estate sales fell 10.9%. On September 30, real estate sales in large and medium-sized cities were -51.5% year-on-year, down from -40.7% in August. Among them, first- and third-tier cities were -52.5%, -53.8%, and -46.5%, respectively, higher than August's -53.2%. , below -37.6% and -37.7%. In September, the land transaction area increased year-on-year.

In September, the land turnover of large and medium-sized cities was 1.6% year-on-year, much higher than the August-7.9% year-on-year. The first-line growth rate rose from 66.3% in August to 66.3%. The second-line rose from -20.6% in August to -13.3. %; the third-line rose from 13.8% in August to 13.1%. In September, the land supply of large and medium-sized cities increased by 57.9% year-on-year, which was higher than that of August, which was 44.3%. The growth rate of land supply in first- and third-tier cities was 523.5%, 50.6% and 26.4%, respectively, which was higher than August's 238.7%. 26.6% and 52.5%.

The passenger car market picked up in August. In terms of retail sales, this year's August growth rate was 6%, which was the same as that in July, which was stronger in the near future. The growth rate of the first five weeks was 14%, 1%, 2%, 5%, and 11%, respectively, and the retail growth rate rebounded. In terms of wholesale, the cumulative growth rate in the first five weeks was 6%, and the wholesale trend in August was relatively smooth. The reason was that the previous destocking efforts were relatively strong, and the dealers’ purchase pressure was small.

Last week, the box office receipts of the movie dropped by 7.5%, and the number of movie visitors and screenings were -7.8% and -2.7% respectively. On a year-on-year basis, box office receipts, movie attendances and screenings in September were 70.4%, 60.4% and 21.9%, respectively, which were lower than 85.0%, 72.8% and 23.1% in August, mainly due to the end of the summer gold file. The demand for viewing of middle school students has dropped rapidly.

The price of textile raw materials increased year-on-year. The yarn price index in China's textile economic information index rose by 0.43% from the previous month to 5.7% in September, up from 4.0% in August. The grey cloth price index rose by 0.21% from the previous month to 1.4% in September, up from 1.1% in August. At the end of August, the price of raw materials, grey cloths, apparel fabrics and home textiles in the Keqiao Textile Price Index increased by 0.45%, decreased by 0.01%, by 0.51%, or by 1.73%, respectively, which was lower than the previous month's 2.76% and higher than last month. 0.61%, lower than 0.69% last month and higher than 1.53% last month.

The container freight index decreased month-on-month and slowed down year-on-year, and the dry-distribution index DBI continued to rise. Last week, the Shanghai Export Container Freight Index (SCFI) fell 2.4% from the previous month and 6.1% from September, far lower than August's 37.8%. China's Export Container Freight Index (CCFI) fell 0.8% qoq, compared with 17.1% in September, down from 21.3% in August. Domestic and international freight prices have increased from the previous month. This week, the Baltic Dry Index (BDI) rose by 5.7% from the previous month to 46.0% in September, far lower than the 69.8% year-on-year in August. Last week, China's coastal dry bulk freight index (CCBFI) rose by 1.0% month-on-month, compared with 22.6% in September, up from 9.5% in August.

|

2, the tour: power generation coal consumption rose, construction machinery sales are booming

This year's power generation coal consumption increased year-on-year. The average daily coal consumption of the six major power generation groups decreased by 8.9%. The average daily coal consumption of the 6 major power generations this month was 697,000 tons, down from 797,000 tons in August. Coal consumption in September increased by 21.8% year-on-year, up from 13.2% in August. In September, the electricity consumption of residents has stabilized, and the correlation between electricity consumption and industrial production has been further strengthened. In September, the construction season has entered, and industrial electricity consumption has increased.

Domestic steel mills' profit ratio last week was 85.9%, which was the same as the previous week's data and remained at a high level. Last week, the national blast furnace operating rate was 76.4%, down 0.8 percentage points, and steel mill production continued to flourish. As of August 20, daily crude steel output increased by 5.3% year-on-year, lower than July's 10.3%. Affected by the “2+26†environmental protection and production restriction measures of Beijing-Tianjin-Hebei, the steel market is expected to continue to rise, driving high rebar fluctuations, up 2.0% on a week-on-week basis, and September rebar prices up 68.1%, up from 61.3% in August. .

The cement price growth rate has slowed down. Cement prices rose 0.4% month-on-week this week, up 24.4% year-on-year in September, down from 27.4% in August. Last week, the national cement storage capacity reached 65.3%, lower than the previous value of 66.0%. September to November is the traditional peak season for the cement industry, with strong downstream demand and tight clinker supply. According to the peak production requirements, the production capacity will be greatly reduced by large-scale shutdown of kiln on November 15. Under multiple benefits, cement prices are expected to enter the autumn up cycle.

The chemical products market is growing steadily. There were 26 kinds of products with rising prices in the chemical sector this week. The top 3 commodities were carbon black (up 3.14%, up 34.48%, up 5.03% from last week), butadiene (1.87% increase from the previous month). , a year-on-year increase of 22.47%, an increase of 1.51 percentage points from the previous week), sodium metabisulfite (upper-quarter growth of 1.62%, an increase of 35.70%, an increase of 15.17 percentage points from last week). There were 6 kinds of products with a decrease in the chain. The top 3 products were propylene oxide (down 2.86%, up 26.62%, down 7.69 percentage points from last week), and fatty alcohol (down 1.69% from the previous month, down 4.88% from the same period of last year). , decreased by 3.36 percentage points from last week, and chloroform (down 0.50% from the previous month, up 28.24% year-on-year, down 5.08 percentage points from last week).

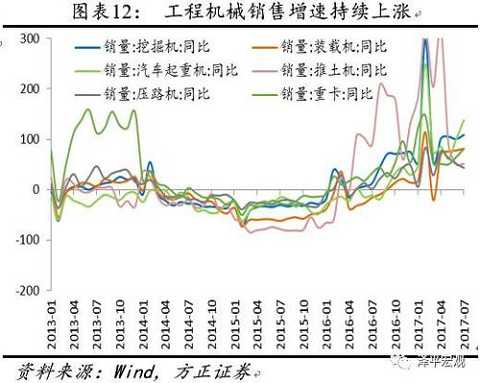

The mechanical market sales have increased significantly. According to the data of the Mining Machinery Branch of China Construction Machinery Industry Association, 91,439 sets of excavation machinery products were sold from January to August, a year-on-year increase of 101.1%. Among them, the domestic market sold 85,576 units, a year-on-year increase of 111.1%; export sales of 5,641 units, a year-on-year increase of 17.8%. Since the beginning of this year, excavator sales have continued to maintain high growth. On the whole, various factors such as infrastructure pull, replacement demand, low base effect last year, and export growth have combined to provide momentum for continued high growth in sales of excavators this year.

|

|

3 , upstream: oil prices fluctuate upwards, strong color

This week, CRB industrial raw materials index was 0.5% from the previous month, and 13.6% from September, up from 12.0% in August. The South China Industrial Products Index decreased by 0.2% from the previous month to 49.0% in September, up from 41.4% in August. The South China Agricultural Products Index was up by 0.7% from the previous month, up from 2.9% in August, up from 2.4% in August.

The Trump administration's "sloppy" move to introduce the US-South Korea FTA has caused panic in the market. Inflation is "far below". Fed director Leonard has published dovish remarks, which has caused the market to expect a rate hike from the Fed. The unexpected rate hike, Fed Vice Chairman Fisher left, the dollar hit a double blow, the dollar index continued to fall. This week, the US dollar index fell by 0.7% month-on-month, compared with -3.1% in September, down from -2.3% in August. The US debt ceiling issue has entered a "countdown" phase, and the dollar has fallen under pressure. Stimulated by the fall of the US dollar, gold bulls hedged, gold prices rose slightly, this week, London spot gold rose 1.98%, compared with 0.56% in September, up from -3.98% in August.

In terms of crude oil, the refining of some refineries in the US, which was discontinued in the previous period, raised the demand for crude oil. The Russian oil minister hinted that the price reduction agreement would be extended again, and the price of crude oil fluctuated. This week, Brent crude oil rose by 2.7% from the previous month and 12.5% ​​from September, up from 10.0% in August. Cloth oil hit a new high since May 25, and the increase was expanded to 1.5%, surpassing the $54 mark. US oil rose above $49/barrel, an increase of more than 0.7%.

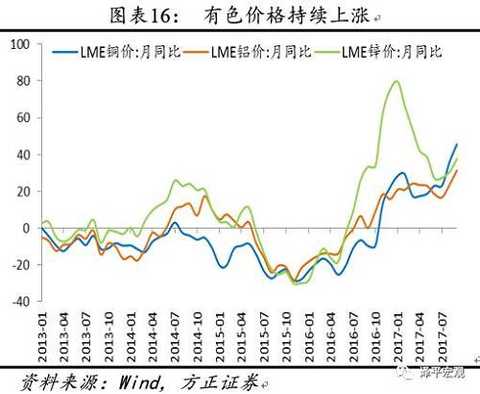

Non-ferrous prices continue to rise. LME copper was down 1.3% this week, compared with 45.5% in September, up from 36.1% in August. LME aluminum prices fell by 2.1% on a week-on-week basis, compared with 31.5% in September, up from 23.7% in August. LME zinc prices were 1.9% on a week-on-week basis, compared with 37.6% in September, up from 30.6% in August.

|

4 , the price : vegetable prices stabilized, pig prices flattened, oil prices stabilized drug prices continue to fall

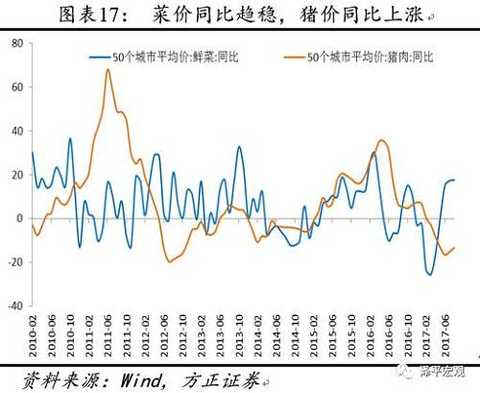

This week, the average wholesale price of 28 key vegetables monitored by the Ministry of Agriculture increased by 0.5%, the Qianhai Vegetable Wholesale Price Index rose by 2.7%, and the Shandong Vegetable Wholesale Price Index fell by 0.4%. With the end of the high temperature, vegetable prices began to fall back. The average wholesale price of 28 key vegetables for monitoring in the Ministry of Agriculture, the wholesale price index of Qianhai vegetables and the wholesale price index of vegetables in Shandong were -0.4%, -5.8% and 0.2% respectively in September, which were lower than 4.5% in August. 1.0%, 13.8%.

The average wholesale price of pork in the Ministry of Agriculture this week was 0.0%, compared with -17.8% in September, up from -19.6% in August. The average retail price of pork in 36 cities fell by 0.1% month-on-month, compared with -9.2% in September, up from -9.9% in August. The National Development and Reform Commission issued the "Analysis of the price of pigs in the first half of the year and the analysis of the later trend", warning that the supply of pork in the second half of the year may increase further, and the overall price of pigs will still decline. The average retail price of beef and mutton in 36 cities was 0.3% and -2.0% respectively in September, which was higher than -0.2% and -2.4% in August. The average retail prices of aquatic products and flowers in 36 cities were 6.04% and -2.06%, respectively, in September, which were higher than and lower than 5.78% and 7.99% in August.

In the non-food sector, oil prices were stable and drug prices continued to fall. On September 1, the National Development and Reform Commission announced that the price of refined oil products in the country will not be adjusted. The unadjusted amount will be added or offset when it is included in the next price adjustment. China's Chengdu Chinese herbal medicines price index was 7.5% in September, down 0.9 percentage points from August's 8.4%.

|

5. currency: the exchange rate continued to strengthen the financial side loose short end of the interest rate downward

This week, the central bank's open market has a total of 370 billion reverse repurchase due, from Monday to Wednesday, respectively, expired 140 billion, 70 billion, 160 billion, Thursday and Friday, no reversible repurchase, and there are 169.5 billion MLF on Thursday. Period, no repurchase and central bank bills expired.

On Monday and Tuesday, a total of 210 billion reverse repurchase expires. The central bank will withdraw funds of 210 billion yuan for open market operations. On Wednesday, the central bank restarted 28 days of reverse repurchase operations and launched 40 billion yuan in the open market. In the reverse repurchase operation, the 7-day and 28-day varieties each have 20 billion yuan, and the net return capital is 120 billion yuan. On Thursday, the central bank conducted a one-year 298 billion yuan MLF operation, with a bid rate of 3.2%, which was the same as last time.

The MPA assessment in the third quarter is just around the corner. The central bank has restarted the 28-day reverse repurchase in the past three months, which is conducive to the market's smooth cross-assessment. At the same time, the incremental MLF is continued, and the market's stable intention is obvious. The funding pattern will be eased in August. .

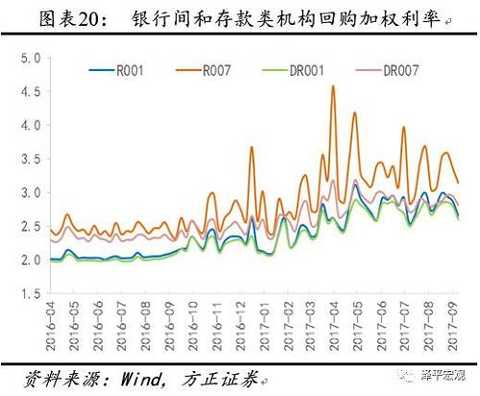

As of September 7, the 1-day inter-bank repurchase plus rights ratio was 2.6543%, down 20.85 BP from last week; the 7-day inter-bank repurchase plus rights ratio was 3.1391%, down 21.83 BP from last week. The 1-day deposit-type institutions repurchase rights plus rights ratio was 2.5961%, down 19.69 BP from last week; the 7-day deposit-type institutions repurchased plus rights ratio was 2.8116%, down 12.92 BP from last week. The one-year government bond yield was 3.5062%, up 11.53 BP from last week; the 10-year bond yield was 3.6554%, up 2.01 BP from last week.

The direct interest rate (monthly interest rate) of the Pearl River Delta Bill and the direct interest rate (monthly interest rate) of the Yangtze River Delta Bill decreased by 2 BP from the previous week, and the bill transfer rate (monthly interest rate) increased by 3 BP. This week's credit differential differentiation for different periods, the credit spread of 1-year AAA corporate bonds fell by 14.15 BP, and the credit spread of 10-year AAA corporate bonds rose by 0.43 BP.

The US dollar index was lower and the RMB exchange rate continued to strengthen. This week, the US dollar appreciated by 0.98% against the central parity of the yuan, the US dollar against the RMB spot exchange rate rose by 0.66%, and the offshore RMB appreciated by 0.30%. The onshore and offshore RMB exchange rate spreads fell from -0.0072 last week to -0.0167, and the US dollar against the RMB 1-year foreign exchange forward purchase price fell by 25 BP.

|

Print Caps,Printed Baseball Caps,Floral Baseball Cap,Leopard Print Baseball Cap

Shandong Urelia International Co., Ltd. , https://www.ureliacaps.com